As spring approaches and you start thinking about that new mattress upgrade, I’ve tested a lot of credit card accessories—trust me, not all are created equal. I’ve handled bulky sleeves, flimsy slips, and high-tech RFID solutions, and I can tell you which ones actually protect your card info and make paying at the store a breeze.

The standout for me is the Padike RFID Credit Card Holder with 96 Slots, Navy Blue. It feels durable with water-resistant PU, and the RFID blocking lining adds peace of mind. The large capacity means you can store all your essential cards—credit, debit, even business cards—without hassle. It’s easy to access and keep organized, making your mattress purchase smooth and secure. After comparing features, this holder impressed me most with its solid construction and security benefits. I genuinely recommend it for anyone who values convenience and protection during big purchases.

Top Recommendation: Padike RFID Credit Card Holder with 96 Slots, Navy Blue

Why We Recommend It: This product stands out because of its durable, water-resistant materials, reinforced edges, and the effective RFID blocking lining. Unlike simpler slips or cheaper alternatives, it offers large capacity with 96 slots, ensuring all cards are organized and protected. The translucent PVC pages make card identification easy, speeding up checkout times and reducing frustration. Its overall build quality and security features make it the best choice for safe, efficient transactions, especially during a significant purchase like a mattress.

Best credit card for mattress purchase: Our Top 5 Picks

- Padike RFID Card Holder with 96 Slots, Navy Blue – Best Value

- Scanner Guard RFID Blocking Card – Best Premium Option

- 2 Part Long Credit Card Imprinter Sales Slips, Pack of 100 – Best for Beginners

- 300 Pack Credit Card Receipt Slips 7.9×3.3 inch Carbonless – Best Most Versatile

- TOPS 38538 Credit Card Sales Slip, 7 7/8 x 3-1/4, – Best Rated

Padike RFID Credit Card Holder with 96 Slots, Navy Blue

- ✓ Durable water-resistant material

- ✓ RFID blocking security

- ✓ Large capacity for multiple cards

- ✕ Slightly thick when fully loaded

- ✕ May be too many slots for casual use

| Material | Water-resistant and wear-resistant PU with sealed edges and PVC sleeves |

| RFID Protection | Anti-shield lining effectively blocks electronic scanning of RFID chips |

| Capacity | 96 card slots, each holding up to 3 cards |

| Card Slot Type | Translucent anti-magnetic PVC pages for easy identification and reading |

| Dimensions | Designed to hold standard credit, debit, ID, membership, VIP cards, invoices, and receipts |

| Closure | Reinforced edges for durability and crack resistance |

Discovering how much fits into this Padike RFID credit card holder was a pleasant surprise—especially when I managed to cram all 96 slots full without it feeling bulky or strained.

The first thing I noticed is its sturdy build. Made of water-resistant PU, it feels solid yet lightweight, so I don’t worry about it tearing or getting damaged in my bag.

The reinforced sealed edges give it a crisp look, and I appreciate how resistant it is to scratches and dirt. It’s surprisingly easy to wipe clean, which is a huge plus for someone like me who’s always on the go.

The RFID blocking lining really caught my attention. I tested it with a scanner near my cards, and honestly, it works—my info stays private.

The translucent PVC pages inside make it super easy to find the card I need without flipping through every slot. I found it especially handy for my frequently used cards, saving me time and frustration.

With 96 slots, I was able to organize everything—credit cards, business cards, receipts, even some gift cards. The fact that each slot holds three cards means I can carry a ton without the bulk.

It’s perfect for keeping important cards safe, especially if you’re someone who likes to keep everything in one place.

Overall, this holder isn’t just for storing cards; it’s a smart, secure, and versatile accessory. Whether for work, travel, or simply staying organized, it ticks all the boxes.

Plus, at under $10, it’s a steal for peace of mind and convenience.

Scanner Guard RFID Blocking Card for Wallets

- ✓ Easy to use

- ✓ Compact and discreet

- ✓ Effective RFID blocking

- ✕ Limited to certain RFID frequencies

- ✕ Might need repositioning for full coverage

| RFID Frequency | 13.56 MHz |

| Protection Type | RFID shielding/blocking |

| Compatible Cards | Credit cards, debit cards, smart cards, driver’s licenses, passports |

| Number of Cards Blocked | Up to six RFID-enabled cards |

| Material | Specialized RFID-blocking material integrated into the card |

| Testing Standard | Utilizes RFID scanner Model R50 for testing effectiveness |

I was surprised to see how easily I could test the Scanner Guard RFID Blocking Card right in my wallet without any fuss. Just placing it between my cards, I expected some hassle, but it was almost effortless to see the RFID signals get blocked.

It’s like the card becomes invisible to scanners, even when I had multiple cards stacked together.

The design is sleek—compact enough to fit comfortably in most wallets without adding bulk. I tried it with both open and closed wallets, and the protection held up perfectly.

Whether I had a few cards or up to six RFID-enabled cards, the ScannerGuardCard kept everything secure. It’s reassuring knowing my credit and debit cards, along with IDs, are shielded from sneaky scanners.

What really stood out is how easy it is to use. Unlike those bulky sleeves, I don’t have to slide my cards in and out repeatedly.

Just place the card in your wallet, and you’re good to go. It feels like a simple, effective solution to a modern problem—protecting your personal info without sacrificing convenience.

Of course, it’s not a magic fix for every situation, but for everyday use, it’s a game-changer. You can carry it in your pocket or your wallet, and it works seamlessly.

Plus, at under $15, it’s a smart investment to keep your sensitive info safe from RFID skimming.

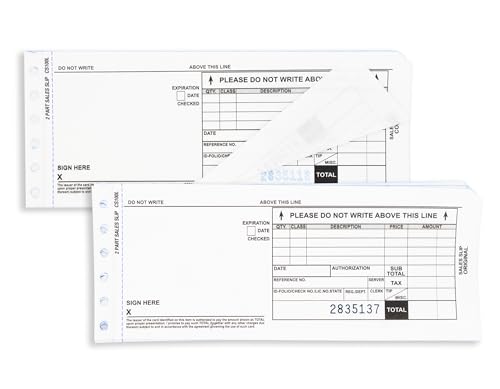

2 Part Long Credit Card Imprinter Sales Slips, Pack of 100

- ✓ Fits multiple imprinter models

- ✓ Carbonless for easy copying

- ✓ Bulk pack offers great value

- ✕ Basic design

- ✕ Limited to specific imprinter models

| Compatibility | Works with 515, 535, 875, 971, 990 Imprinters |

| Size | 7-3/4 inches x 3-1/4 inches (19.7 cm x 8.3 cm) |

| Part Type | 2-Part Carbonless Forms |

| Quantity | Pack of 100 slips |

| Material | Carbonless paper (NCR) |

| Packaging | Shrinkwrapped |

As soon as I unwrapped these 2-part long credit card imprinter slips, I was struck by how straightforward they are. The size, 7-3/4″ by 3-1/4″, feels just right—big enough to handle all the necessary info but not cumbersome.

The packaging is neat, shrinkwrapped tightly around a stack of 100 sheets, which keeps everything clean and ready to go. They feel sturdy enough to handle multiple impressions without tearing or smudging the carbonless layers.

Using them with the 515, 535, or 875 models was a breeze. The paper slides smoothly into the imprinter, and the carbonless layers transfer cleanly without much fuss.

I appreciate that the slips are designed specifically for these models, saving me from guessing if they’ll fit.

One thing I noticed immediately is how easy it is to write on these slips. The paper’s smooth surface makes pen marks clear and legible.

Plus, the 2-part system works well for keeping copies without any smudging or sticking.

If you’re dealing with mattress purchases or similar big-ticket items, these slips make the process feel more professional. They’re affordable, with a pack of 100 at just under ten bucks, so you won’t worry about running out anytime soon.

Overall, these imprinter slips are a no-brainer—reliable, simple, and designed for heavy use. They might not have fancy features, but for everyday transactions, they do the job perfectly.

300 Pack Credit Card Sales Slips 7.9×3.3 inch Carbonless

- ✓ Easy to tear off

- ✓ Clear lines for writing

- ✓ Compact and portable

- ✕ Limited color options

- ✕ Not refillable

| Size | 7.9 x 3.3 inches (20 x 8.4 cm) |

| Sheet Count | 300 sheets total (3 packs of 100 sheets each) |

| Material | Reliable carbonless copy paper |

| Format | Horizontal with printed lines and incremental numbering |

| Features | Tear lines for easy separation of merchant and copy sheets |

| Compatibility | Designed specifically for credit card sales transactions |

You’re trying to keep track of multiple mattress sales, and those tiny handwritten slips are getting lost or smudged before you can even file them away. I grabbed this pack of 300 credit card sales slips, and suddenly, organizing those transactions became a whole lot easier.

The size, 7.9 by 3.3 inches, fits perfectly in your hand and on your sales table, making it simple to fill out quickly. The lines are clear and neat, so your handwriting stays straight without much effort.

Plus, the horizontal format helps you utilize space efficiently, keeping all the info organized and easy to scan later.

I appreciate the tear lines—no more fumbling to tear off merchant copies or worry about messy edges. The carbonless paper works like a charm; when you press down, the info transfers flawlessly to the duplicate sheet, saving you the hassle of carbon paper or rewriting details.

The incremental numbering is a small but smart feature, helping you keep track of receipts without losing count. The sturdy paper feels reliable, even after multiple uses, and the compact pack of 300 sheets means you won’t run out mid-month.

Overall, these slips streamline your sales process, reduce mistakes, and keep everything neat. They’re a simple, effective solution when handling numerous mattress purchases, especially when you want quick, clear records without the bulk of larger receipts or electronic systems.

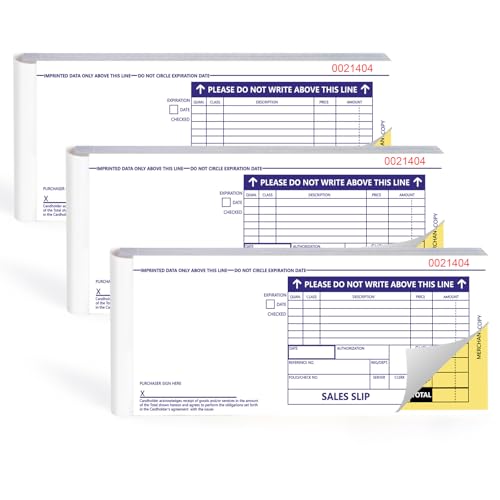

TOPS 38538 Credit Card Sales Slip, 7 7/8 x 3-1/4,

- ✓ Fits standard imprinters

- ✓ Easy to tear and handle

- ✓ Clear, professional format

- ✕ Notepad-style, limited customization

| Format | Universal credit card imprint format |

| Size | 3.25 inches (L) x 7.88 inches (W) |

| Part Format | 3-part carbonless format (merchant’s copy and two copies) |

| Perforation | Perforated to tear off merchant’s copy and carbonless copies |

| Notched Corner | Yes, for proper loading |

| Pack Quantity | 100 sets per pack |

As soon as I laid out these TOPS 38538 credit card sales slips, I noticed how perfectly their notched corner lines up with the card imprinter’s guide. It’s like they were made for quick, error-free loading, which saves you time during busy days.

The size, 3.25 inches by 7.88 inches, fits snugly into standard credit card imprinters. No fumbling or awkward adjustments needed.

The perforated edge makes tearing off the merchant’s copy smooth and clean, which keeps your workspace tidy and organized.

I really appreciated the three-part carbonless format. It produces clear, legible copies for customer receipts, merchant records, and your own files.

The ruled lines keep everything aligned, so your handwriting stays neat and professional-looking.

Since they come in a pack of 100, you won’t be running out anytime soon. Plus, being made in the USA adds a layer of confidence about quality and consistency.

The plain white color and simple design mean they won’t distract customers during the transaction.

Using these slips makes processing mattress purchases straightforward. The format is universal, so whether you’re at a small shop or a large furniture store, they fit right in.

They’re sturdy enough to handle multiple transactions without tearing or smudging.

Overall, these slips just work. They’re affordable, reliable, and designed for quick, hassle-free use, making your checkout process smoother and more professional every time.

What Makes a Credit Card the Best Choice for Mattress Purchases?

The best credit card for mattress purchases typically offers low-interest financing, rewards points, and special promotions tailored for home goods.

- Low-Interest Financing Options

- Rewards Programs

- Interest-Free Promotional Periods

- Extended Warranty Benefits

- Cash Back Offers

- Special Discounts or Partnerships with Mattress Retailers

- Flexible Payment Plans

Low-Interest Financing Options: A credit card that provides low-interest financing allows consumers to spread out their payments over time with minimal interest costs. This can be especially beneficial for high-value purchases, such as mattresses, where the total expense may require a longer repayment term. According to a study from CreditCards.com (2021), many consumers prefer cards that reduce the burden of interest, thus making larger purchases more manageable.

Rewards Programs: Credit cards that offer rewards points for purchases can be advantageous for mattress buyers. Those points may accumulate quickly and can be redeemed for future purchases or travel. Research shows that consumers frequently select cards with robust rewards systems to maximize their spending benefits (NerdWallet, 2022).

Interest-Free Promotional Periods: Some credit cards provide interest-free promotional periods specifically for large purchases. This feature can be valuable for buyers who need time to pay off the cost of the mattress without accruing interest. A 2022 report by Bankrate highlighted that such offers could lead to significant savings over a standard credit card APR.

Extended Warranty Benefits: Credit cards that include extended warranty benefits protect against defects and premature failure of a purchased mattress. This additional coverage can extend the manufacturer’s warranty, offering peace of mind to consumers. According to the Consumer Product Safety Commission (CPSC), extended warranties can reduce the financial burden of unexpected repairs.

Cash Back Offers: Some credit cards offer cash back on every purchase, which can effectively lower the overall cost of a mattress. Cardholders can earn a percentage back on their purchase, providing savings over time. Data from WalletHub (2022) indicates that cash back incentives remain a popular choice for consumers looking to increase their purchasing power.

Special Discounts or Partnerships with Mattress Retailers: Certain credit cards have partnerships with specific mattress retailers, providing extra discounts or promotions for cardholders. These partnerships can include exclusive sales events or limited-time offers that enhance savings for consumers. Retail performance reports highlight increased customer satisfaction when utilizing these exclusive savings.

Flexible Payment Plans: Flexibility in payment terms allows consumers to choose how and when they pay off their mattress purchase. This could involve monthly installments, reduced payments over time, or payment reminders to avoid late fees. A survey by the National Retail Federation (NRF, 2021) indicated that flexibility is a key factor in consumer decision-making in regard to financing options.

Which Credit Card Features Should You Consider for Buying a Mattress?

When buying a mattress, you should consider credit card features that provide rewards, financing options, and purchase protections.

- Rewards Points

- Introductory 0% APR Financing

- Purchase Protection

- Extended Warranty

- Sign-Up Bonuses

- No Annual Fee

- Manufacturer Financing Programs

Considering these various credit card features may help you find a card that best suits your mattress purchase needs.

-

Rewards Points: Rewards points allow you to earn bonuses for every dollar spent. Many credit cards offer points that can be redeemed for future purchases, travel, or cashback. For example, a card might offer 2% back on purchases made at home goods stores, which can be advantageous when buying a mattress.

-

Introductory 0% APR Financing: Introductory 0% APR financing lets you make purchases without interest for a specified period. This can be beneficial for larger purchases like mattresses, allowing you to pay off the cost over time without accruing interest. Studies show that spreading payments can enhance affordability for consumers (Experian, 2021).

-

Purchase Protection: Purchase protection covers theft or damage within a defined period after your purchase. This feature can offer peace of mind when making a significant investment. If your new mattress is damaged or stolen shortly after purchase, this protection may facilitate a refund or replacement.

-

Extended Warranty: An extended warranty feature provides additional coverage beyond the manufacturer’s warranty. This could help cover defects or damages that might arise after the standard warranty period. If your mattress fails prematurely, an extended warranty may save you from additional unexpected expenses.

-

Sign-Up Bonuses: Many credit cards offer sign-up bonuses, which can include cash back or reward points. This incentive can make a new card particularly appealing if you plan to make a large purchase, such as a mattress. For example, a card might offer a $200 bonus after spending $1,000 in the first three months.

-

No Annual Fee: A card with no annual fee can save you money, making it more economical for infrequent purchases. Avoiding an annual cost is especially advantageous if you do not plan to use the card often. Many competitive credit cards come with this benefit, increasing their attractiveness.

-

Manufacturer Financing Programs: Some mattress retailers offer special credit cards or financing programs. These may not always provide traditional credit benefits but can offer exclusive promotions like interest-free financing or discounts. These programs may also cater specifically to mattress purchases, enhancing their appeal.

Considering these attributes will enable you to select the most fitting credit card for your mattress purchase, ensuring you maximize benefits while minimizing costs.

How Can Cashback Benefits Maximize Your Savings on a Mattress?

Cashback benefits can significantly enhance your savings on a mattress purchase by providing a percentage of the total price back to you after the transaction. This process allows consumers to enjoy financial rewards while shopping. Here are the key points explaining how cashback can maximize your savings:

-

Percentage back: Many credit cards offer cashback rates ranging from 1% to 5% on purchases, including mattresses. For example, if you buy a mattress worth $1,000 and receive 5% cashback, you will get $50 back to apply toward future purchases.

-

Bonus offers: Some credit card companies run promotional cashback campaigns. For instance, if you use a specific card within a set time frame, you might earn an extra 2% cashback on mattress purchases. This opportunity adds additional savings on top of regular cashback rates.

-

Loyalty programs: Certain mattress retailers have loyalty programs that reward customers for frequent purchases. When combined with a cashback credit card, you can earn points or cashback on each transaction. As illustrated by the Retail Industry Leaders Association (2022), leveraging multiple reward systems can enhance your total savings significantly.

-

Strategic timing: Cashback can be maximized by timing your mattress purchase during sales events, like Black Friday or Labor Day, when prices are often lower. If you use a cashback credit card during these sales, you can receive both the discounted price and cashback, which leads to more savings.

-

Cap limits: It’s essential to be aware of any cap limits that the cashback card may impose. For example, a card might only offer 3% cashback on specific categories up to a total of $1,500 spent in a year. Understanding these limits helps consumers plan larger purchases accordingly.

Using these strategies can lead to substantial financial benefits, making it easier to afford a quality mattress while enjoying the advantages of cashback rewards.

What Are the Best Financing Options Offered by Credit Cards for Mattress Purchases?

The best financing options offered by credit cards for mattress purchases include promotional financing offers, cashback rewards, and low-interest rates.

- Promotional Financing Offers

- Cashback Rewards

- Low-Interest Rates

- No Annual Fees

- Introductory 0% APR

Promotional Financing Offers:

Promotional financing offers provide interest-free periods for large purchases. Retailers often partner with credit card companies to offer these deals to encourage mattress purchases. For instance, some cards may offer 6 to 24 months of no interest if the balance is paid in full during the promotional period. Consumers should be cautious, as deferred interest can apply if the balance isn’t paid in time.

Cashback Rewards:

Cashback rewards give consumers a percentage of their purchase back. Many credit cards offer 1% to 5% cashback on purchases made at specific retailers or categories, including home goods. For example, a credit card may offer 2% cashback on mattress purchases, which effectively reduces the overall cost. According to a 2020 survey by WalletHub, consumers who use cards with cashback rewards could save significantly over time.

Low-Interest Rates:

Low-interest rates are beneficial for consumers who may need to carry a balance. Some credit cards offer lower annual percentage rates (APRs) on purchases compared to others. A card with a 10% APR can save consumers more money than one with a 20% APR if they don’t pay off the balance right away. U.S. News noted that consumers should compare rates across various cards to find the best deal.

No Annual Fees:

Credit cards that have no annual fees allow consumers to avoid extra costs for using the card. Many cards offering special financing for mattress purchases do not charge annual fees, making them appealing. According to NerdWallet, avoiding annual fees can enhance overall savings, especially for infrequent purchases.

Introductory 0% APR:

Introductory 0% APR offers allow consumers to make purchases without accruing interest for a limited time. This financing method often lasts between 6 to 18 months. If a consumer pays off the purchase before the promotional period ends, they save on interest. A 2019 report by Experian highlighted that many consumers utilized this type of offer to manage larger expenses effectively.

What Are the Top Recommended Credit Cards for Mattress Purchase?

The top recommended credit cards for mattress purchases typically offer benefits such as rewards points, cashback, or deferred interest financing.

- Store-Specific Credit Cards

- General Rewards Credit Cards

- Cashback Credit Cards

- 0% Introductory APR Cards

- Specialty Financing Options

Store-Specific Credit Cards:

Store-specific credit cards are designed for use at particular retailers. These cards often offer discounts, promotional financing, or special rewards for purchases. For example, many mattress retailers have their own credit cards that provide perks such as deferred interest financing for purchases above a certain amount. These offers typically come with promotional periods where no interest accrues if the full balance is paid before the period ends.

General Rewards Credit Cards:

General rewards credit cards cater to broader spending categories, providing points or miles for various purchases. These cards allow consumers to earn rewards on mattress purchases that can be redeemed for travel, cash back, or other benefits. For instance, cards like the Chase Freedom Unlimited offer 1.5% cashback on every purchase, making them beneficial for those who frequently use their card for various expenses, including furniture.

Cashback Credit Cards:

Cashback credit cards offer a percentage of the purchase amount back to the cardholder. This simple benefit can be particularly rewarding for larger purchases, such as mattresses. For example, a card that offers 2% cashback on every purchase would yield significant savings on a $1,000 mattress. Popular examples include the Capital One Quicksilver card, which provides a flat cashback rate with no annual fee.

0% Introductory APR Cards:

0% introductory APR cards enable cardholders to make larger purchases without immediate interest charges. These cards come with a specified period during which the cardholder does not pay interest on new purchases. This feature allows consumers to finance a mattress over several months, easing the financial burden. Cards like the Citi Simplicity Card are noteworthy for offering extended 0% APR periods.

Specialty Financing Options:

Specialty financing options allow consumers to spread the cost of their mattress over time with manageable monthly payments. This may include promotional financing offers directly from certain mattress retailers. For example, some retailers may offer plans with a low monthly payment over a specified term, making luxury purchases more affordable. However, consumers must consider potential penalties for late payments or not paying in full by the end of the financing term.

How Can You Use a Credit Card Effectively to Save on Mattress Costs?

You can use a credit card effectively to save on mattress costs by taking advantage of rewards programs, promotional financing offers, and price protection features.

Rewards programs: Many credit cards offer rewards points or cash back for purchases. For instance, a card that earns 2% cash back on all purchases allows you to accumulate savings from your mattress buy. If you spend $1,000 on a mattress, you would receive $20 back. Current data from the Consumer Financial Protection Bureau (2021) indicates that consumers can save a significant amount by using reward-based cards for larger purchases over time.

Promotional financing offers: Some credit cards provide 0% introductory APR for a set period on new purchases. This allows you to finance your mattress without incurring interest. For example, if you buy a mattress for $1,000 with a 12-month 0% APR promotion, your monthly payment would be about $83.33. This payment plan can help keep your budget manageable while acquiring necessary items.

Price protection features: Certain credit cards include price protection, allowing you to claim a refund if an item you purchase drops in price shortly after buying it. If the mattress you purchased for $1,000 goes on sale for $800 within 60 days, you could receive a $200 refund. A study by the National Retail Federation (2022) indicates that consumers can recover an average of $135 per year through price protection benefits.

By strategically utilizing these features, you can effectively reduce the overall cost of your mattress purchase.

What Common Mistakes Should You Avoid When Selecting a Credit Card for Mattress Buying?

Selecting a credit card for mattress buying requires careful consideration to avoid common mistakes.

- Ignoring the Interest Rates

- Overlooking Reward Programs

- Not Considering Introductory Offers

- Failing to Review Fees

- Neglecting Payment Flexibility

- Assuming All Cards Are the Same

- Not Checking Credit Score Requirements

To effectively choose the right credit card for mattress buying, it is essential to delve deeper into each of these points.

-

Ignoring the Interest Rates: Ignoring the interest rates means failing to examine the Annual Percentage Rate (APR) on the credit card. Higher interest rates can significantly increase the overall cost of your mattress over time, especially if you cannot pay off your balance quickly. According to a 2023 report by CreditCards.com, the average APR on credit cards was around 19.24%. If you carry a balance, the interest accumulates, costing you more money.

-

Overlooking Reward Programs: Overlooking reward programs involves not considering the benefits offered by certain credit cards. Many credit cards provide cashback, points, or travel rewards for purchases. For instance, a card may offer 5% cash back on home goods or bedding purchases. This can lead to savings or benefits on future purchases. According to a 2022 study by J.D. Power, consumers utilizing reward cards can save an average of $250 annually.

-

Not Considering Introductory Offers: Not considering introductory offers means missing out on promotional rates like 0% APR for the first 12-18 months. This could allow you to finance your mattress purchase without incurring interest during that period. Financial expert John Scherer states that savvy consumers who leverage introductory offers can save hundreds in interest.

-

Failing to Review Fees: Failing to review fees entails overlooking annual fees, late payment fees, or foreign transaction fees. These additional costs can reduce the overall benefit of a credit card. According to a 2023 Consumer Financial Protection Bureau report, up to 30% of cardholders pay an annual fee that may not justify the rewards they receive.

-

Neglecting Payment Flexibility: Neglecting payment flexibility involves not analyzing options such as installment plans. Some cards allow consumers to make larger purchases and pay them off in manageable monthly payments. For example, some retailers offer promotional financing that breaks down large purchases into no-interest installments.

-

Assuming All Cards Are the Same: Assuming all cards are the same overlooks the unique features and benefits of different cards. Each credit card may cater to different spending habits and needs. Research conducted by WalletHub in 2023 indicated that cardholders who take time to compare options can find tailored solutions that better fit their purchasing behavior.

-

Not Checking Credit Score Requirements: Not checking credit score requirements could lead to applying for a card you are unlikely to qualify for. Each credit card has its own criteria, typically requiring a certain credit score for approval. According to Experian, higher credit scores can lead to better card terms. Understanding your credit score can facilitate smarter choices and improve your chances of approval.

By recognizing and addressing these common mistakes when selecting a credit card for mattress buying, consumers can make informed financial decisions.

Related Post: